Table of Content

Primary residences are owner-occupied, principal residences only. Second home properties must be owner-occupied at some point during the year. While there are plenty of resources that explain what a home equity line of credit is and what you can use it for, you’re not alone if you still have questions.

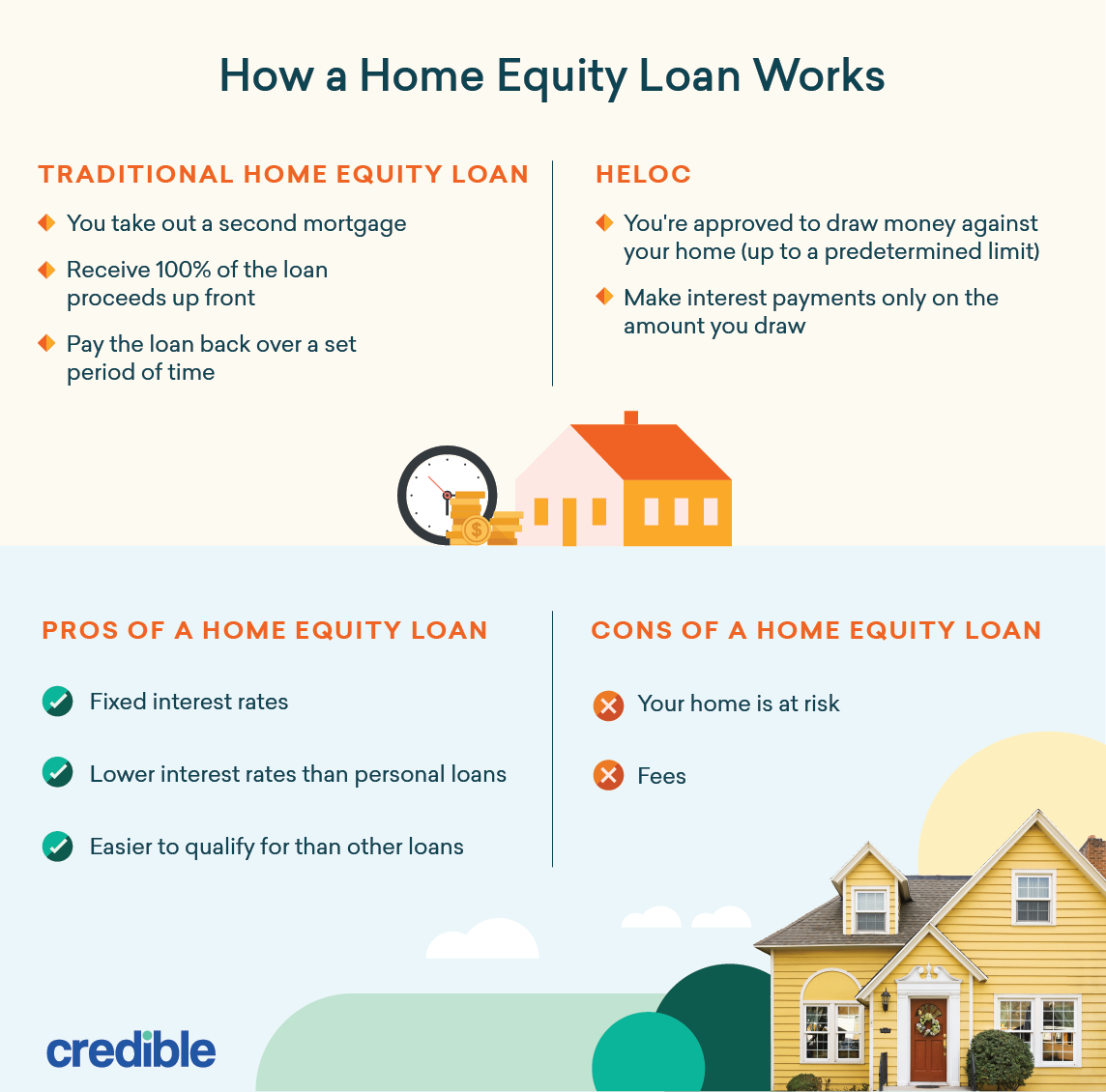

For co-ops, additional terms and conditions will apply. For a property value greater than $2.5 million, additional terms and conditions may apply. If you’ve worked hard to build equity in your home by making mortgage payments over time, you might be thinking that it's time to put that equity to good use.

Easy application

A HELOC is the easiest way to access a home’s equity and can provide borrowers with several benefits. A homeowner with a home valued at $500,000 may have paid $200,000 of their principal. If their HELOC lender allows them to borrow up to 85% of the home’s value, they will multiply $500,000 by 0.85 to determine they can borrow a maximum amount of $425,000. That maximum, minus the $300,000 they still have to pay off on their mortgage, means they can acquire a HELOC for up to $125,000. Disaster often strikes without warning, and when it happens to your health, the expensive medical bills you’re left with could necessitate a loan. An unsecured emergency loan is one option, but a fixed-rate HELOC may be cheaper and easier to pay off.

Payments may change based on your balance and interest rate fluctuations, and may also change if you make additional principal payments. Making additional principal payments when you can will help you save on the interest you’re charged and help you reduce your overall debt more quickly. You should also be aware that most HELOCs have variable rates, meaning the interest rate you pay will change with fluctuations in the market.

Helping You Get Down to Business.

Choosing an interest-only repayment may cause your monthly payment to increase, possibly substantially, once your credit line transitions into the repayment period. Repayment options may vary based on credit qualifications. Loans are subject to credit approval and program guidelines. Not all loan programs are available in all states for all loan amounts. Interest rates and program terms are subject to change without notice.

HELOC’s come with their own interst rate, and borrowers will pay back the interest just like they would on a mortgage or credit card payment. Interest rates for HELOCs are adjustable, meaning they can change with the market. HELOC interest rates typically remain close to mortgage rates. 3 ALEC will waive closing costs up to $500 for fees that include title insurance and recording fees. Minnesota applicants are responsible for a mortgage registration tax.

Home Equity Line of Credit (HELOC) Special | Apply Online

At Bank of America®, we want to help you understand how you might put a HELOC to work for you. A HELOC is a line of credit borrowed against the available equity of your home. Your home's equity is the difference between the appraised value of your home and your current mortgage balance. If you want to have only one loan on your property and one mortgage payment to make each month. Cash-out refinances also typically come with more attractive rates, since they’re a first mortgage and are therefore less risky. For those who have their current loan with us, you can do an FHA cash-out transaction with a 580 median FICO® Score as long as you're paying off debt at close.

The Ultimate Certificate Strategy Laddering your certificates is an excellent way to ensure you earn the best rates possible. A home equity line of credit is a flexible and affordable way to cover large, ongoing or unexpected expenses, like home improvements and debt consolidation. A home equity loan is a consumer loan allowing homeowners to borrow against the equity in their home. First, of course, you will have to have equity to borrow against. Bear in mind that lenders won't let you borrow the full amount of your equity but will generally limit you to no more than 85% of it.

When the draw period ends, the repayment period begins, and it’s your responsibility to pay off the balance before the maturity date. To secure a HELOC, borrowers must start by filling out an application. Typically, HELOCs banks, credit unions, and other financial institutions work with homeowners. Applying for and receiving approval for a HELOC can take several weeks, so potential borrowers should prepare to wait before they can begin accessing their funds. HELOCs consider the amount of equity that a homeowner has in their home and allows them to tap into the equity they’re building.

They will have to make a minimum interest-only payment each month but should also entertain the idea of paying back part of the principal to avoid a higher balloon payment down the line. Additionally, paying down the principal frees up more potential funds that homeowners can access again should they need them in the future. Keep in mind the risks involved when using your home as collateral. If you can’t pay the money back, you could lose your home to foreclosure. Talk to an attorney, financial advisor, or someone else you trust before you make any decisions. Some dishonest lenders target older adults, homeowners with modest means, and borrowers with credit problems.

The interest rate you’ll get for any debt you take on will vary depending on your own financial situation and what the economy is doing at the time. You should also be careful about using a HELOC to pay for everyday expenses. Though it might start to feel like a regular credit card, you’re trading valuable equity for the money you borrow from your HELOC. In general, it’s best to only use your HELOC for things that will help you financially, such as boosting the value of your home or paying for higher education. The first phase, called the draw period, is when your line of credit is open and available for use. During this period, you’ll be allowed to borrow from your line of credit as needed, making minimum payments or possibly interest-only payments on the amount you’ve borrowed.

That might be useful, for example, if you plan to remodel your kitchen this year and add on a deck in a year or two. Both home equity loans and home equity lines of credit are based on the difference between your home's current value and how much you still owe on your mortgage. To qualify for a HELOC, you need to have available equity in your home, meaning that the amount you owe on your home must be less than the value of your home. You can typically borrow up to 85% of the value of your home minus the amount you owe.

No comments:

Post a Comment